For those wondering what is likely to happen in the financial markets this year the “bet” seems pretty simple. There was $9.2 trillion of stimulus in 2020, three times the size of 2008 when the world almost toppled. With the Democratic sweep, there will be yet more stimulus, perhaps higher than 2020 itself. The excess liquidity in the system is so epic in proportion that if any of us believe that we will emerge from the fear and (self)-loathing of lockdown, then inflation has arrived. The conversation can no longer be about achieving inflation targets but how far out of control it will get.

Last year, the virus – the outbreak (Jan/Feb), the first lockdown (March/April), the second wave (June/July), and then the rolling lockdowns, until now, have completely dominated the tone of the market and we have in some ways, underestimated the power of government and social media – the strongest powers on earth. For the former, the appearance of zero rates, populism and the motive to maintain power was powerful and for the latter, the opportunity for economic gain was unparalleled. For those smart enough to play the game it was a good year.

This letter cannot be about our view on Covid except to say we still think its effects have been overdone and we are deeply sad that so many have been left in a catatonic state of fear, virtual life and home delivery. Our only point is that the UK government is the gilt-tipped edge of stupidity. Straight from today’s Google, it is very easy to toggle between cases and deaths to see that the BBC is feeding us with untruths and that it has chosen not to see this incorruptible data: cases are 12 times higher than the Spring peak but deaths are roughly half the peak. Hmm.

We realise our take on this is different and that debating something that has created so much fear is pointless. Here is what is relevant: our expectation was that the proof that an extremely significant increase in testing did not result in even close to a concomitant rise in deaths would allay concerns and that on recognition of multiple vaccines, the market would begin to discount the other side of this pandemic. In fact, whilst value, read cyclical sectors, have risen they outperformed for just two solitary days after the excellent Pfizer efficacy data.

Obviously, there are some questions to ask: Why didn’t the market want to discount the vaccine?

We would guess upon a few unproven reasons: increased testing, more cases and significant lockdowns, doubts over the vaccine, Jerome Powell’s toxic display of bubble encouragement (“We are not even thinking about thinking about raising rates”), the obsession with technology, – Bitcoin and green thematic investing – but mostly because it was year-end, a time of good will in which to collectively support your fellowman. In modern day terms this meant agreeing to ignore information and keep buying the same asset classes in which everyone had a vested interest.

Looking forward, what do we think are the ramifications and opportunities?

It is February 2021 and vaccinations en masse have started. A momentum bull (think anyone exposed to anything long duration e.g. Bonds, Large cap U.S. Indices, “Growth” Sectors – Technology, ESG etc.) could, perhaps hang on to the concept that the entire population will not be vaccinated for a few months, perhaps the summer but front-line workers, the most-at-risk and elderly will be pretty soon.

More than 13 million people in the UK have already received the first dose of the Covid-19 vaccination…

It is simply too close to an end to not want to position for the other side.

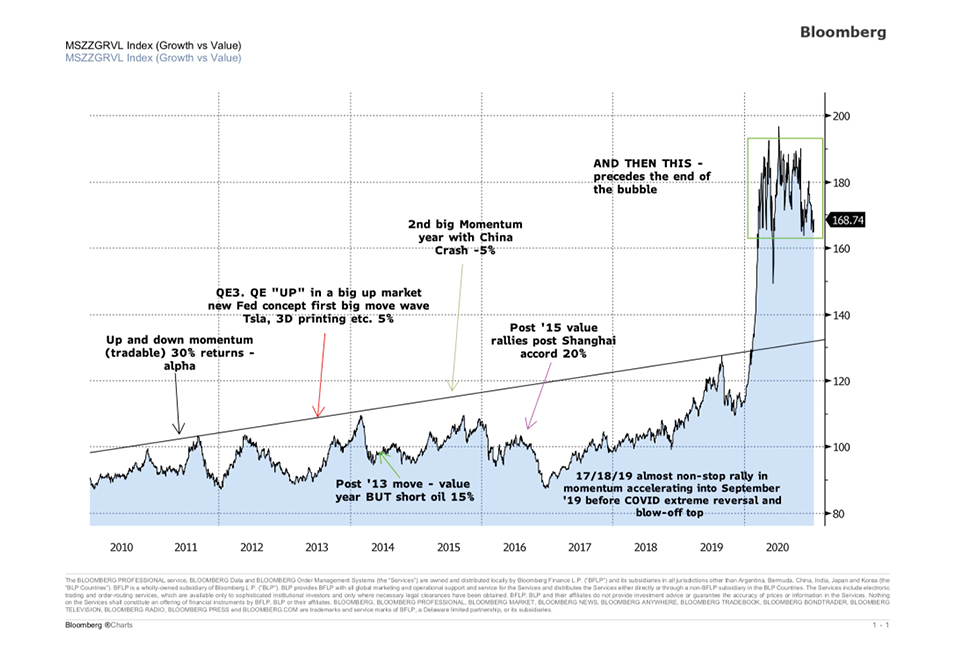

We believe that inflation will drive a seismic shift in investment portfolios out of bonds, growth stocks, tech stocks and into deep value (energy, financials, cyclicals). But wait, after the longest bull market in history and proliferation of passive investing, isn’t this “The Market”, where all of your investments and pensions are exposed…

We are at the end and turning point of a 40-year cycle. Of course, there have been many bubbles but the bubbles observable every day now makes everything and anything that have been seen in the past look negligible. The Covid pandemic has created an epic blow-off top in markets and if you were in any doubt as to the fragility of markets look no further than the, at best bizarre and at worst damn right dangerous, speculative fever that has hit U.S. equity markets in recent weeks. Bidding up worthless companies to stratospheric valuations all in the name of “sticking it to the man” with the added irony that this is being encouraged by nefarious actors (technology billionaires) posing as “men of the people”, is beyond comprehension.

This, in our view, is the bubble to end all bubbles and it is likely to pop sometime around economic normalization and a taper tantrum sometime in 2021. It is possible that our shorts crash down while inflation protected sectors (energy / financials / uranium) crash up. We can but dream but there is genuine logic to this.

Any unwind of the lockdowns, post clarity on the Congress and the House and post Brexit, is going to cause a travel boom and an economic reflation that could perhaps look quite violent in trajectory. Will this happen next month? Seemingly not but can we start to preview it for Q2/Q3, one quarter out. This is the bet and our best guess on the timing which of course could be off. There is no room for complacency here so we will trade around this view until we see the whites of its eyes.

ABOUT THE AUTHOR:

Richard is a Portfolio Manager at Trefoil Capital Advisers Ltd. Richard has over 28 years of investment experience. Having graduated with a 1st Class Honours degree from Leeds University with Distinction in Economics and Modern Languages Richard joined Morgan Stanley before heading Global Hedge Fund sales at Prudential Securities. In 2005 Richard joined SAC Capital as a macro strategist and research trader. In 2010 Richard joined Carlson Capital where he was a partner and Portfolio Manager of the award winning, multi-billion dollar Black Diamond Thematic Fund.

Show Comments +